WEDNESDAY, 10 APRIL 2024

Analysing Prime London Housing Market – Spring Edition

With increased instructions and decreased fall-throughs, we have seen a positive start to the 2024 property market. While the £5m+ Prime Central London sales market has returned to normal activity levels following two strong years, values remain 26.1% above 2017-19. The data used in this report comes from three designations: Prime Central, Prime Inner, and Prime Fringe.

For the Prime Central London lettings market, there was an annual fall of lets agreed, but an increase in new instructions to indicate positive months ahead.

Entering Spring and Q2, a traditionally busy period for property, we explore the London real estate market.

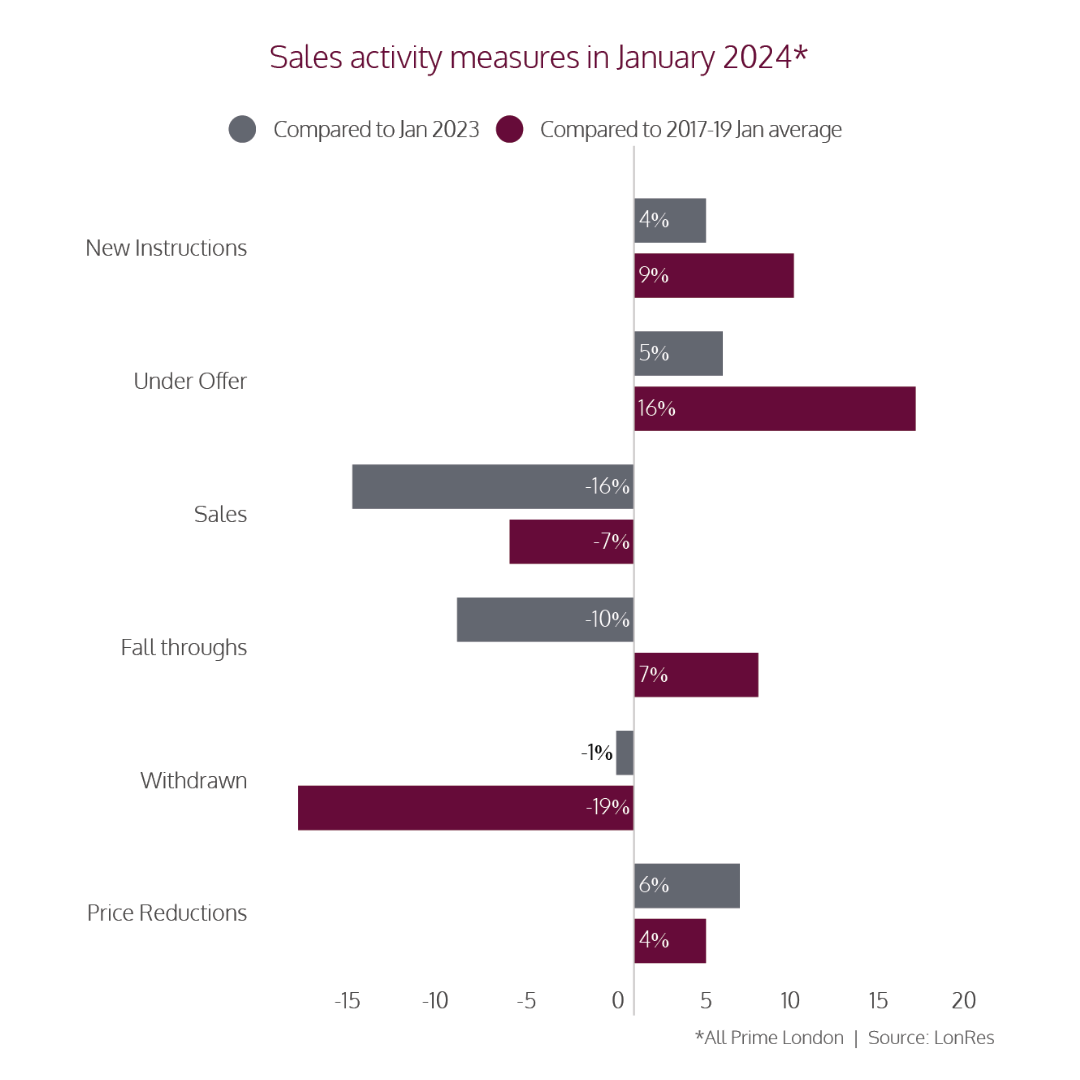

– In January 2024, the number of properties under offer grew by 5.4% annually

– Fall through and withdrawals in January were lower than in 2023

– House prices are only 0.8% higher than in 2014

– Overall, on average, prime London fringe grew by 18.3%

(Source: LonRes)

A Positive Start

With Spring on the horizon, we see positive signs in the sales and lettings property market. In January, the number of properties under offer grew by 5.4% annually. During this period, instructions increased by 4.2%. The volume of for-sale stock at the end of January was 5.4% higher than the previous year.

Achieved prices fell to -7.1% in January, the most significant drop in five years. However, properties under offer have a brighter outlook. LonRes reports an annual increase of 5.4%, increasing levels to 15.6% above the average pre-2019.

Fall-throughs and withdrawals in January 2024 were lower than the previous January, and price reductions were just 6% higher. These metrics indicate a healthy market.

Trends Over The Decade

House prices are only 0.8% higher than in 2014. However, there has been a fluctuation throughout London neighbourhoods. New transport links and housing developments bolstered some areas, while others have remained the same.

At just 3.1%, Prime Central London has witnessed the least growth in price. South Kensington saw -2.5% and Chelsea 0.9%. However, some neighbourhoods here thrived. Mayfair and St James saw 20.7% growth.

For inner prime, Fitzrovia, Bloomsbury and Soho have seen a change of 32.6%. Other neighbourhoods experienced a rise, too. Kensington, Notting Hill & Holland Park saw a hike of 26.2% and Hampstead 29.3%. The overall average for prime inner was 18.9% growth.

For prime fringe, Vauxhall, Nine Elms, Borough & Kennington have experienced a 28.8% increase, possibly boosted by the extension of the Northern Line, regeneration and new homes. Overall, on average, prime fringe grew by 18.3%.

With the rise in mortgage rates, buyers may be priced out of Prime Central London and move to fringe and inner London. The addition of new transport links will make areas in the prime inner and prime fringe more connected and desirable. For example, the Northern Line extension, the introduction of the Elizabeth Line and the planned extension of the Bakerloo Line, opens up new places to live.

A report by Zoopla made predictions for the coming year stating, “we expect market conditions in London to continue to improve over 2024, with earnings rising faster than house prices. This will continue to improve affordability and support levels of housing sales rather than boost house prices.”

The £5m+ Market

In January, activity in the £5m+ market slowed down. However, transaction levels remain ahead of historical trends. While sales were 17% lower than in January 2023, they remained 64% higher than the January 2017-2019 average.

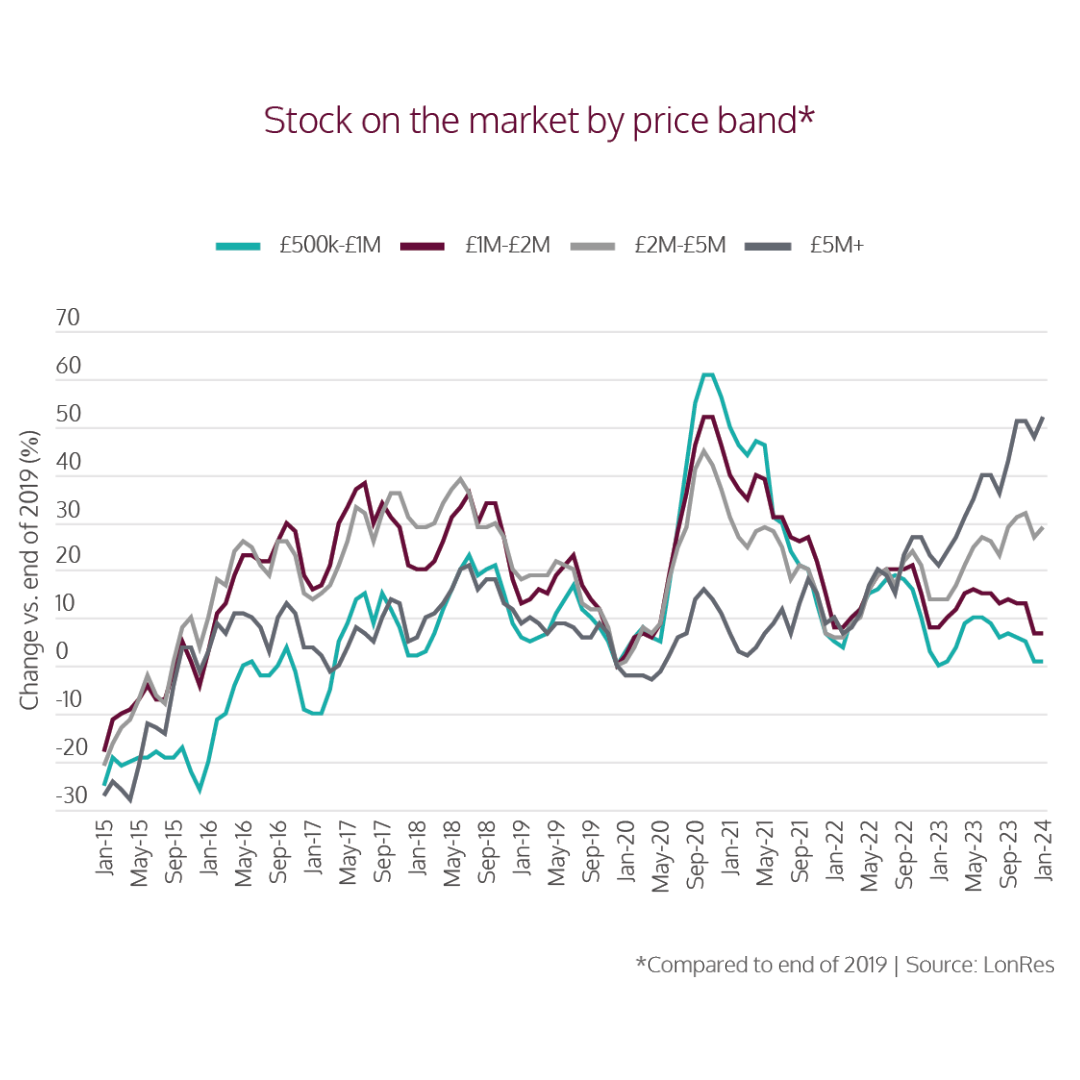

The supply of premium London homes priced at £2-5m+ is increasing. In January 2024, new instructions were 42% higher than the same month in 2023 and 148% higher than January 2017-2019. New instructions for homes priced at £500k-£1m are falling.

Rental Growth

While rental values remain 26.1% higher than their 2017-2019 average, annual rental growth fell to 3.1% in January. Data from LonRes indicated a yearly fall of 11.5% in lets agreed, which is 60.8% below the January 2017-2019 average.

However, instructions for properties to rent in London rose by 22.1% in January 2024. While fewer houses are on the prime London rental market than in 2020, the increase in instructions presents a positive sign.

Buy-to-let mortgages are at the lowest levels since September 2022. With the hike in the Bank of England base rate, buy-to-let mortgages peaked at 6.79% in August 2023. In February 2024, the average fell to 5.5%. While it’s still higher than the 3.06% of February 2022, it’s a move in the right direction.

Planned legislation updates will force landlords to increase the EPC rating of their investment properties. By doing this, landlords may be eligible for green mortgages that offer lower rates and cashback.

In the second quarter of 2020, with reduced demand for rental properties across central London during lockdowns, the value of flats and houses fell. Houses picked up again quickly, and in Spring 2021, they were back to their January 2020 level. Flats remained 15% below. In 2022, the growth gap closed, but since then, the flat premium has fallen to 6%.

Moving Into Spring

As we move into Q2 and Spring, we are seeing the market moving in a positive direction.

While transactions in January were 15.5% lower than in January 2023, the increase in properties under offer is a positive sign. Property prices have increased throughout Prime Central, inner, and fringe, with Prime Inner seeing the most significant average.

If you’re interested in the prime London housing market and properties for sale in London, contact our Central London estate agents team to start a conversation.

The analysis for this report takes in the three LonRes catchment areas:

PRIME CENTRAL

South Kensington

Mayfair & St James’s

Knightsbridge & Belgravia

Kensington, Notting Hill & Holland Park

Chelsea

PRIME INNER

St Johns Wood, Regents Park & Primrose Hill

Pimlico, Westminster & Victoria

Marylebone & Medical Territory

Hampstead

Fitzrovia, Bloomsbury & Soho

PRIME FRINGE

Vauxhall, Nine Elms, Borough & Kennington

Hammersmith & Brook Green, Chiswick, North Kensington

Fulham & Earls Court

Bayswater & Maida Vale

Battersea, Clapham & Wandsworth